What Happens to Your Fixed Income Investments When Central Banks Change Rates?

Central bank rate decisions are often discussed in terms of borrowing costs and the broader economy. However, they also have a direct impact on how fixed income investments behave and that impact can be reflected in portfolio values as rates begin to move.

Unlike products such as GICs, which provide a fixed return when held to maturity, bonds are priced in the market. This means their value can change over time, even if the final outcome at maturity remains the same. As a result, when central banks adjust interest rates, the effect on bonds is often more immediate and more visible.

When interest rates increase, bond prices decline. When interest rates decrease, bond prices increase. This is not a short-term market reaction - it reflects how bonds are structured.

Bonds pay a fixed rate of interest. When new bonds are issued at higher yields, existing bonds with lower rates become less attractive by comparison, and their prices adjust downward. When yields decline, the opposite occurs: existing bonds offering higher rates become more valuable, and their prices increase. This relationship applies consistently across the bond market. What differs is the magnitude of the impact.

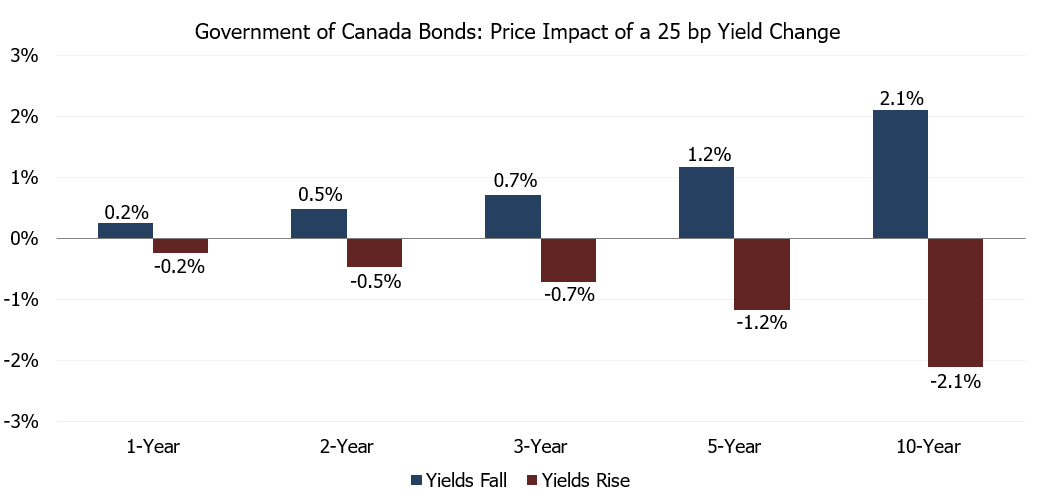

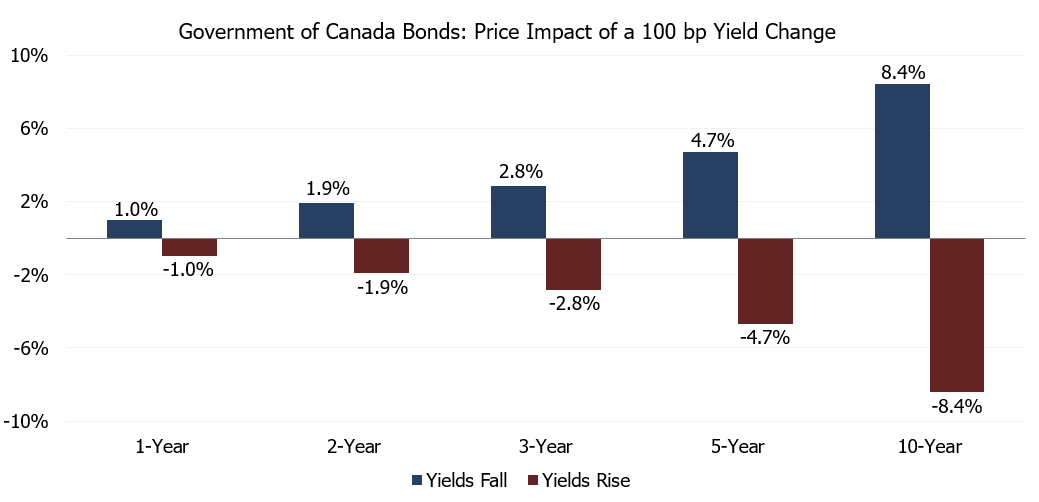

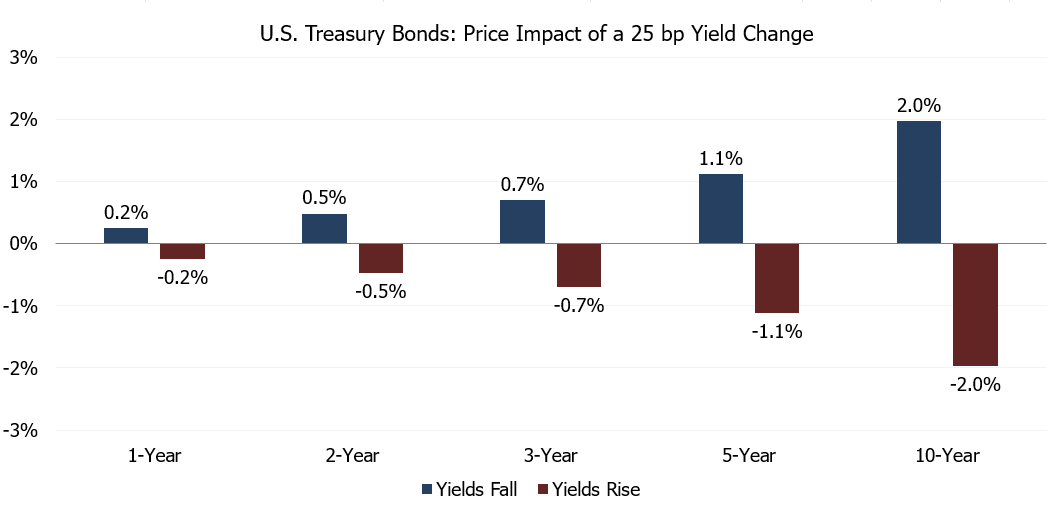

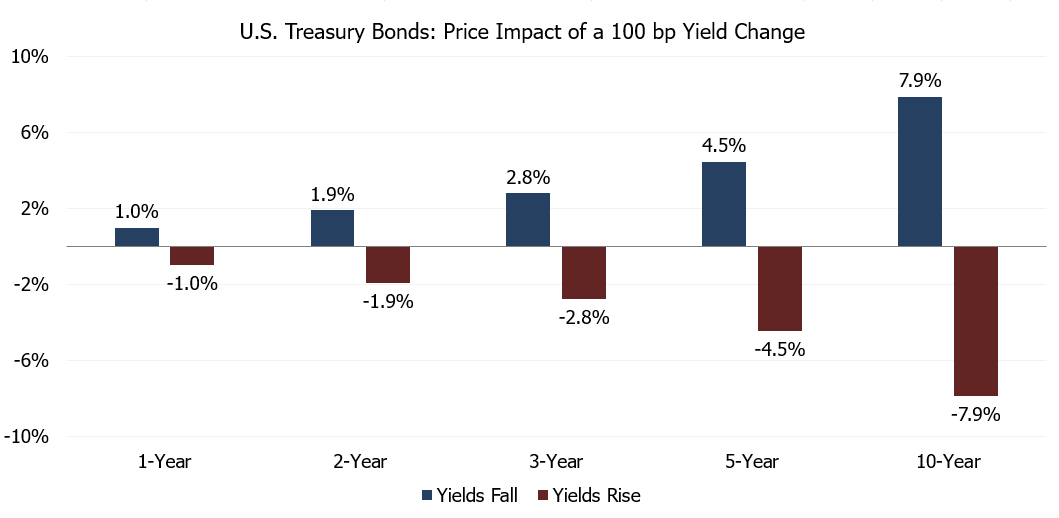

Not all bonds respond in the same way to changes in interest rates. One of the most important factors is maturity. Shorter-term bonds tend to experience relatively small price changes, while longer-term bonds are more sensitive, with price movements becoming more pronounced as maturity increases.

The charts below illustrate this relationship across Government of Canada bonds and U.S. Treasury bonds. A 25 basis point change in yields has a limited impact on a 1-year bond, but a noticeably larger effect on a 10-year bond. When the change in yields is larger, such as 100 basis points, the difference becomes even more apparent. In practical terms, longer-term bonds introduce greater sensitivity to interest rate movements within a portfolio.

Source: Refinitiv. Illustrative price impact based on the modified duration of representative Government of Canada and U.S. Treasury bonds. Actual price changes may vary depending on bond characteristics and market conditions.

This is often where the distinction between bonds and GICs becomes more relevant. Both bonds and GICs provide a fixed return when held to maturity. The difference is not in the final outcome, but in what happens along the way.

For bonds, changes in interest rates matter when purchasing, because they affect the price and yield available in the market. They also matter when a bond is already being held and may be sold before maturity, because its market value will rise or fall as rates change. However, if an individual bond is held to maturity, those interim price changes do not alter its stated interest payments or principal repayment at maturity.

GICs, by contrast, do not have the same price consideration. They do not fluctuate in market value as interest rates change, which means they do not introduce the same visible movement in a portfolio over time. When held to maturity, they provide a stable and predictable outcome.

Understanding how these investments respond to central bank decisions can help explain changes in portfolio values and provide useful context when evaluating fixed income allocations.

If you would like to discuss this further, please contact us at 604.643.0101 or cashgroup@cgf.com.

Book a meeting today with our of our advisors: https://calendly.com/cashgroup-cgf=

Market Updates

Our market commentary breaks down the latest business, financial and money news. If you’d like to receive all of our market update emails, send us an email by clicking the subscribe button. If you found this content helpful, share it widely!