The Disconnect Between Rate Cuts and Borrowing Costs

Borrowing costs have not declined as evenly as many expected, even as central banks have begun cutting interest rates. For households, this has been most noticeable in mortgage rates, which remain relatively elevated despite clear progress on policy easing. The reason lies not only in central bank decisions, but in how bond markets shape financing conditions across the economy.

While policy rates set the direction for interest rates, they do not fully determine how borrowing costs behave in practice. Bond yields across different maturities play a central role in translating policy decisions into real-world financing conditions. This dynamic is particularly relevant for investors in fixed income products such as GICs and bonds, where yields reflect not only central bank actions but also broader market expectations.

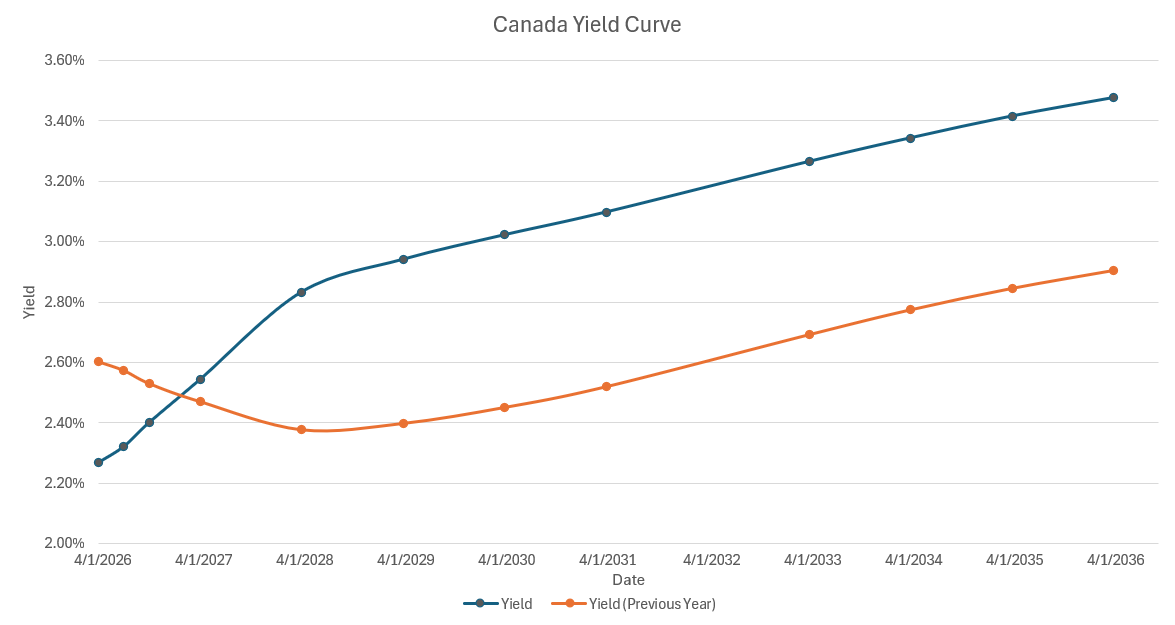

Source: Bloomberg - Data from 03/12/2025 – 03/12/2026

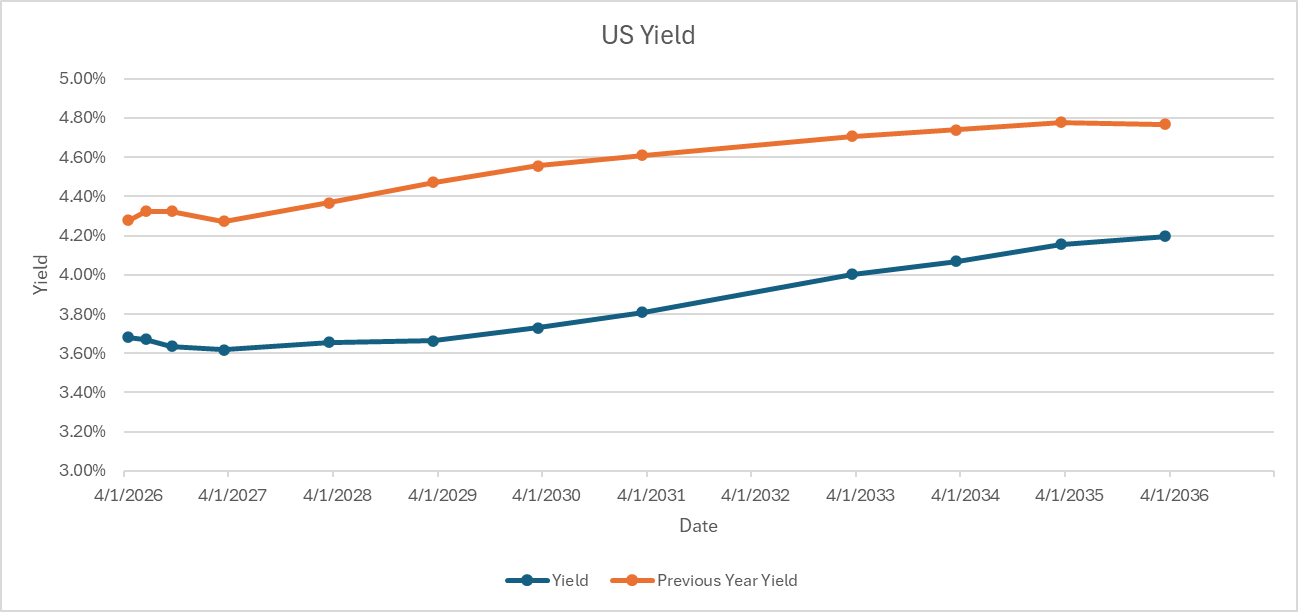

Source: Bloomberg - Data from 03/12/2025 – 03/12/2026

Looking at the Canadian and U.S. yield curves from a year ago, both appeared relatively flat, suggesting that markets were still adjusting to restrictive policy settings and uncertainty around the timing of rate cuts. Notably, the paths of the two curves have since diverged.

In Canada, the Bank of Canada has moved more decisively, cutting its overnight rate to 2.25%, well below the current U.S. policy rate. This has led to a sharper decline in short-term Canadian yields and a steeper yield curve, as earlier policy easing has largely been absorbed at the front end. Longer-term yields, however, have declined more modestly, indicating that while near-term borrowing costs are easing, long-term financing conditions remain more anchored.

In contrast, the U.S. yield curve reflects a more gradual adjustment. Although yields have moved lower, the Federal Reserve’s overnight rate remains higher at 3.75%, and policy easing has progressed at a slower pace. As a result, yields across U.S. maturities remain elevated compared with Canada, shaped by persistent inflation concerns, stronger economic momentum, and broader fiscal considerations. This keeps financial conditions relatively tight, not because policy is being actively tightened, but because higher long-term yields continue to weigh on borrowing and investment decisions.

In practice, this means that central bank rate cuts do not translate directly into lower borrowing costs. Short-term borrowing and variable-rate products tend to respond more quickly to policy changes, which helps explain why some borrowers in Canada have already seen relief. Longer-term borrowing, however, is more closely tied to bond yields further out on the curve, where rates reflect expectations around inflation, growth, and fiscal conditions over time.

For households, this helps explain why mortgage rates have not declined in a straight line. Fixed mortgage rates are influenced by longer-term government bond yields and lender spreads, which can remain stable or even rise if inflation risks or global uncertainty persist. For businesses, similar forces affect the cost of issuing longer-term debt or refinancing existing loans, keeping interest expenses elevated.

For investors, this environment also helps explain why longer-term yields may remain attractive in certain segments of the bond market, even as short-term rates begin to decline.

Taken together, these dynamics highlight that while central bank policy sets the direction for interest rates, it is longer-term bond yields that ultimately determine where borrowing costs settle. Even in a period of policy easing, financing conditions can remain uneven, particularly for longer-term borrowing, as markets continue to price in the broader economic outlook.

At the Cash Management Group, we continue to analyze central bank developments and their implications for clients. By staying ahead of policy shifts and maintaining a flexible, data driven approach, we help institutional and private clients navigate evolving market conditions with confidence.

If you would like to discuss this market update and how it could affect your portfolio, please contact us at 604.643.0101 or cashgroup@cgf.com.

Book a meeting today with our of our advisors: https://calendly.com/cashgroup-cgf

Market Updates

Our market commentary breaks down the latest business, financial and money news. If you’d like to receive all of our market update emails, send us an email by clicking the subscribe button. If you found this content helpful, share it widely!