Market Update: Canada and the US Hold Rates Steady

Both the Bank of Canada and the US Federal Reserve held interest rates steady today, reinforcing a cautious approach to monetary policy as inflation trends, labour markets, and global risks continue to evolve. While economic conditions differ between the two countries, both central banks are facing a similar challenge: inflation has risen again largely due to higher energy prices, while growth and employment remain resilient but are no longer accelerating.

In Canada, the BoC held its overnight rate at 2.25%, signalling that although inflation has moved higher in recent months, underlying price pressures are still expected to ease over time. In the United States, the Fed maintained its target range at 3.50%–3.75%. Notably, the Fed’s decision included multiple dissenting votes, reflecting differing views on how long policy should remain restrictive and when easing should begin, which highlights increased uncertainty around the future rate path.

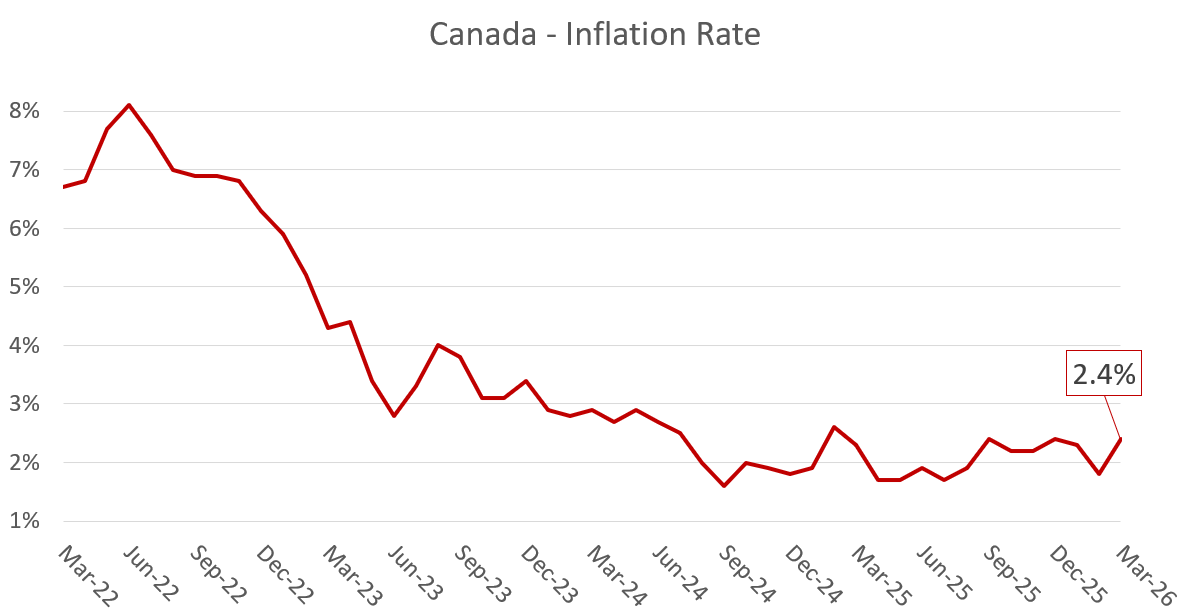

Inflation remains a central focus in both countries, largely driven by higher energy prices amid ongoing geopolitical tensions in the Middle East. In Canada, inflation rose to 2.4% in March, up from 1.8% in February. Excluding gasoline, inflation eased in March, suggesting that broader price pressures remain relatively contained. Energy prices were the key driver, rising sharply on both a monthly and year‑over‑year basis. The Bank of Canada expects inflation to peak around 3% in April 2026, before gradually declining. Assuming oil prices ease as projected, inflation is expected to return to the 2% target in early 2027.

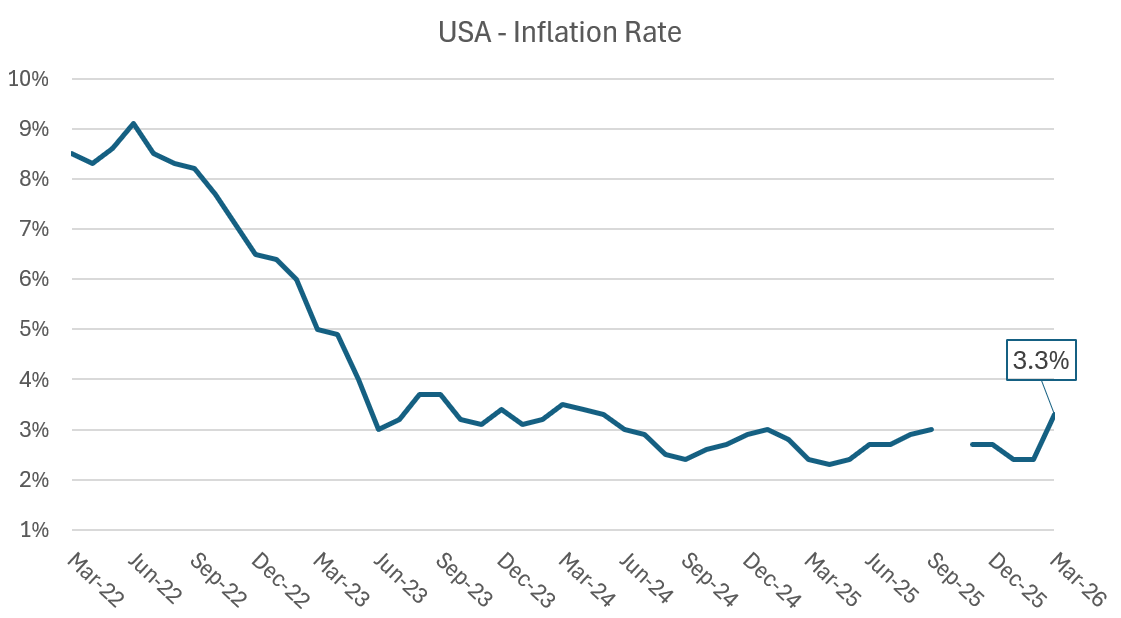

In the United States, inflation increased more sharply, rising to 3.3% in March from 2.4% in February. Energy prices again played a significant role, with the energy index rising more than 12% year over year, while food prices increased at a more moderate pace. Core inflation remains below headline inflation but is still above the Federal Reserve’s 2% target. The Fed has emphasised that the recent increase primarily reflects higher global energy prices rather than a broad re‑acceleration in domestic demand, though the persistence of these pressures remains uncertain.

Source: Statistics Canada - Data from March 2022 to March 2026

Source: U.S Bureau of Labor Statistics - Data from March 2022 to March 2026

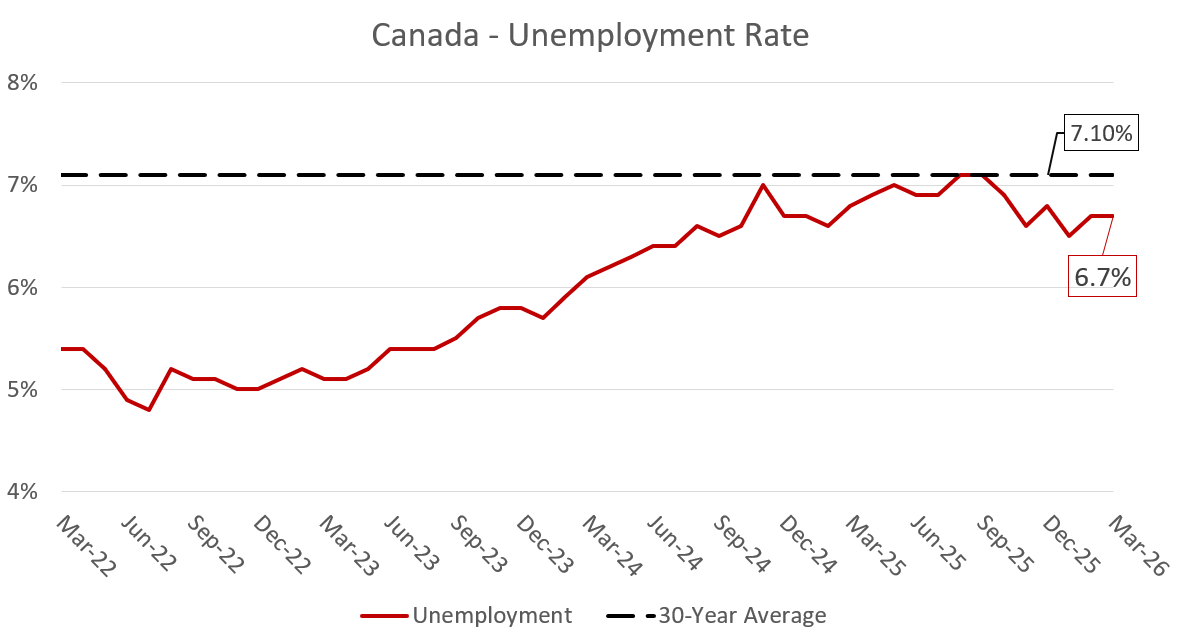

Labour markets in both Canada and the United States remain resilient, though recent data suggest they are no longer a significant source of inflationary pressure. In Canada, employment was little changed in March and the unemployment rate remained steady at 6.7%. Job gains were concentrated in service‑related industries and natural resources, while employment declined modestly in interest‑rate‑sensitive sectors such as finance and real estate. Overall, the labour market appears stable but softening, reflecting slower hiring

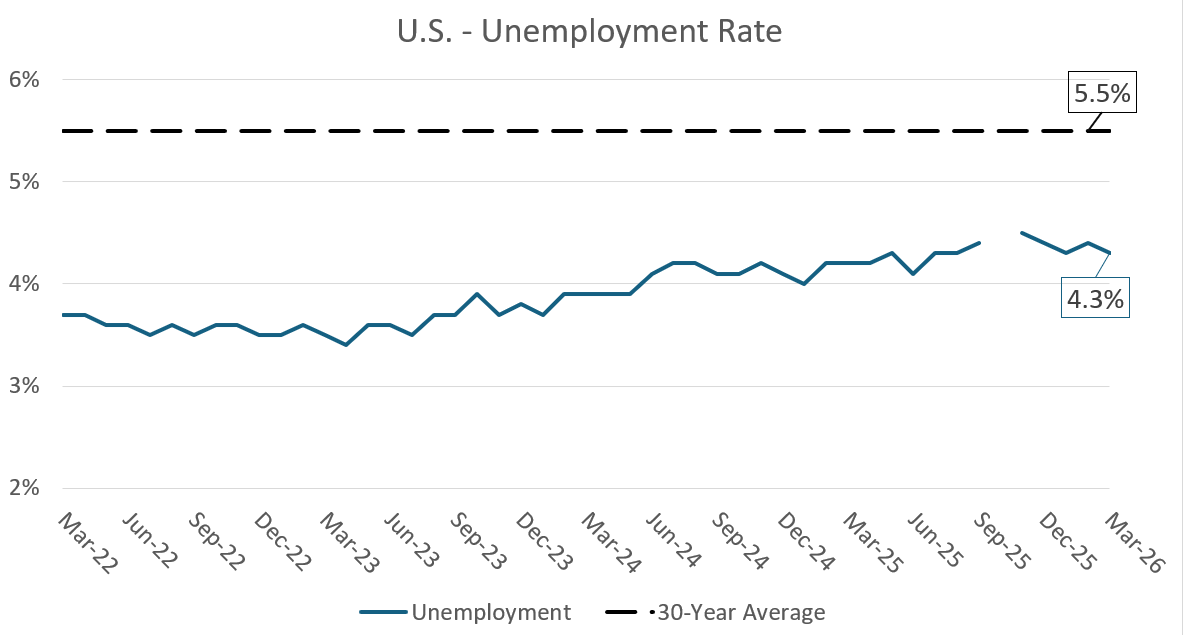

In the United States, non‑farm payroll employment rose by 178,000 in March, and the unemployment rate held at 4.3%. Job growth continued in health care, construction, and transportation, while federal government employment declined. Similar to Canada, this points to a labour market that remains healthy but is cooling, suggesting employment conditions are no longer adding materially to inflation pressures.

Source: Statistics Canada - Data from March 2022 to March 2026

Source: U.S Bureau of Labor Statistics - Data from March 2022 to March 2026

Economic growth remains uneven across the two economies, with the United States maintaining stronger momentum than Canada despite shared global pressures. In Canada, GDP growth is expected to be about 1.2% in 2026, rising modestly to 1.6% in 2027 and 1.7% in 2028. Consumer spending and government investment remain key sources of support, while exports and business investment continue to be constrained by US tariffs and trade uncertainty. Housing also remains a notable drag on growth, as affordability challenges, slower population growth, and excess supply, particularly in parts of the condominium market, limit activity. As a net energy exporter, Canada benefits from higher oil prices through improved national income and government revenues. However, higher fuel and food costs are squeezing household budgets, which tempers the overall boost to growth.

In contrast, the US economy continues to expand at a solid pace, supported by consumer spending, productivity gains, and strong investment—particularly in technology and artificial intelligence. According to the Federal Reserve’s latest projections, US GDP growth is expected to be 2.4% in 2026, 2.3% in 2027, and 2.1% in 2028, modestly above the economy’s longer‑run trend of roughly 2.0%. While momentum has cooled compared to 2025, the overall outlook remains stronger than in Canada. That said, elevated interest rates, higher energy prices, and ongoing geopolitical uncertainty remain key risks to the US outlook.

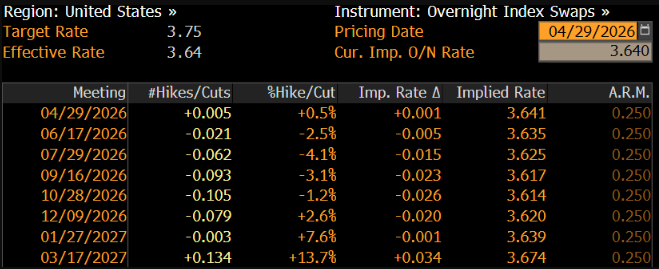

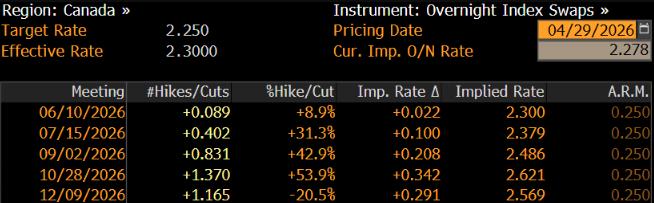

Looking ahead, in the United States, markets are currently pricing in no interest‑rate changes this year, reflecting the Fed’s focus on elevated inflation and ongoing global uncertainty. In Canada, expectations are more finely balanced, with markets assigning roughly a 54% probability of a rate increase later in the year, depending on how inflation and growth evolve.

World Interest Rate Probability - Source: Bloomberg - April 29, 2026

If you would like to discuss how these developments could affect your portfolio, please contact us at 604.643.0101 or cashgroup@cgf.com.

Book a meeting today with our of our advisors: https://calendly.com/cashgroup-cgf

Market Updates

Our market commentary breaks down the latest business, financial and money news. If you’d like to receive all of our market update emails, send us an email by clicking the subscribe button. If you found this content helpful, share it widely!