US Reserve Holds Rates Steady as Inflation Pressures Persist

On June 17th, the US Federal Reserve announced that it is holding its benchmark interest rate unchanged in the target range of 3.50% to 3.75%. The decision marks the first policy announcement under newly appointed Federal Reserve Chair Kevin Warsh and comes at a time when inflation remains above the Fed’s 2% target, while economic activity and labour market conditions continue to demonstrate resilience. At the same time, geopolitical tensions in the Middle East have contributed to higher energy prices, while uncertainty around global trade policy continues to create challenges for businesses, consumers, and investors.

Although the decision to hold rates steady was widely expected, the context behind it is important. The Federal Reserve is continuing to assess whether recent inflation pressures will prove temporary or remain persistent enough to require a more restrictive policy stance. Notably, the Fed removed language from its policy statement that had previously suggested future reductions in borrowing costs, reflecting a more neutral approach to monetary policy. Updated committee projections also revealed a divided outlook among policymakers, with some members expecting rates to remain unchanged while others see the possibility of additional rate increases if inflation remains elevated.

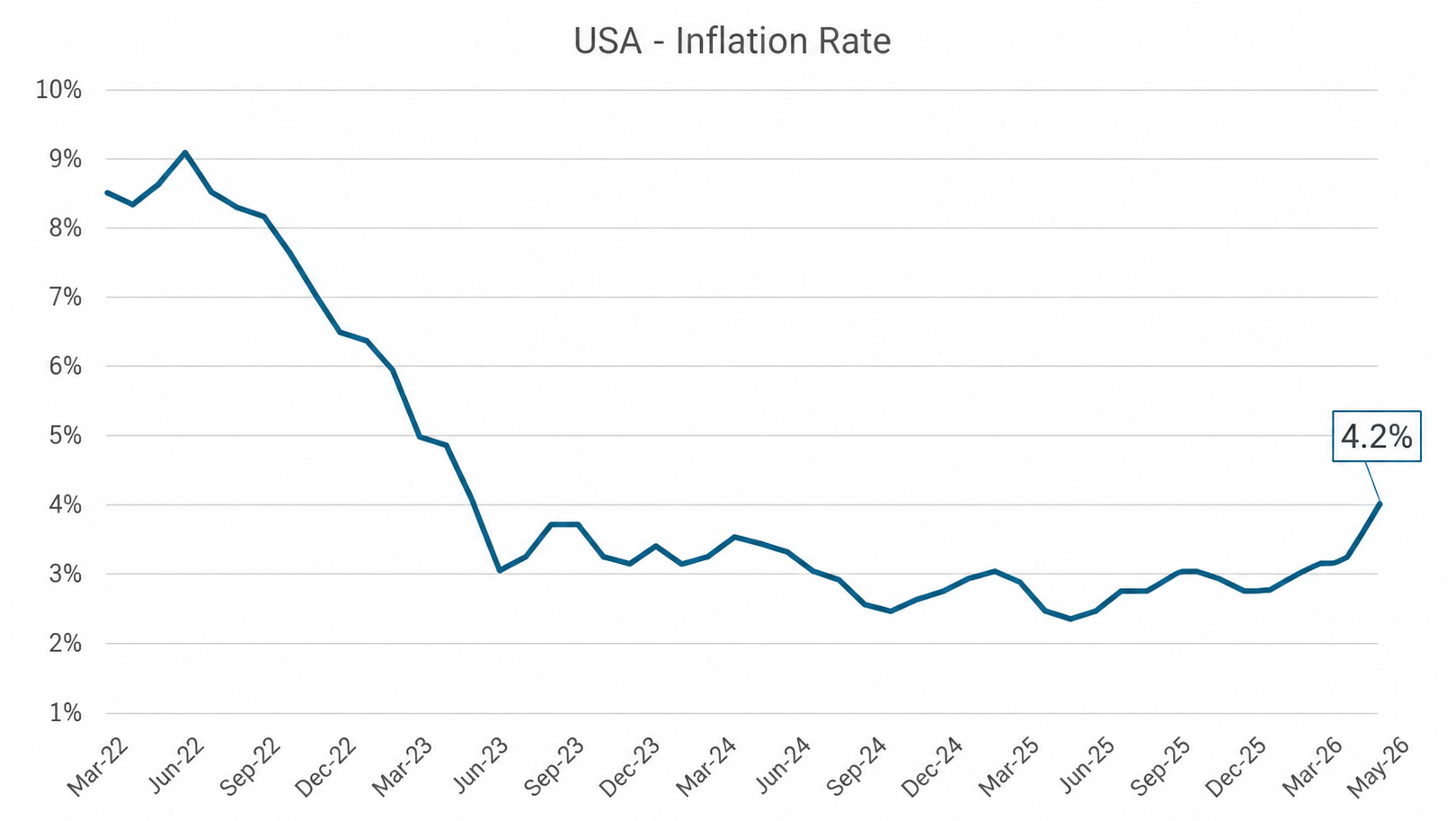

In May, the US Consumer Price Index rose 4.2% compared to a year earlier, while the headline index increased 0.5% during the month. Higher energy prices were a significant contributor to the increase, with energy costs rising 23.5% over the previous year and energy commodities increasing 40.6%. Excluding the more volatile food and energy categories, core inflation was lower at 2.9%, suggesting that broader price pressures remain more contained than the headline figure alone would imply. Food prices increased 3.1% over the year, while shelter costs rose 3.4% and medical care services increased 3.6%. While inflation has declined significantly from the highs reached in 2022, recent data suggests that progress toward the Federal Reserve’s 2% target may be slowing.

Source: U.S. Bureau of Labor Statistics - Consumer Price Index (CPI), March 2022 to May 2026

The broader economy has remained relatively resilient despite higher borrowing costs. Consumer spending continues to support economic activity, while business investment and hiring have remained stronger than many economists anticipated earlier in the year. This resilience has given policymakers flexibility to maintain a restrictive policy stance while they continue evaluating incoming economic data. However, higher interest rates continue to weigh on interest-sensitive sectors of the economy, and policymakers remain attentive to signs that economic growth could slow more meaningfully over the coming quarters.

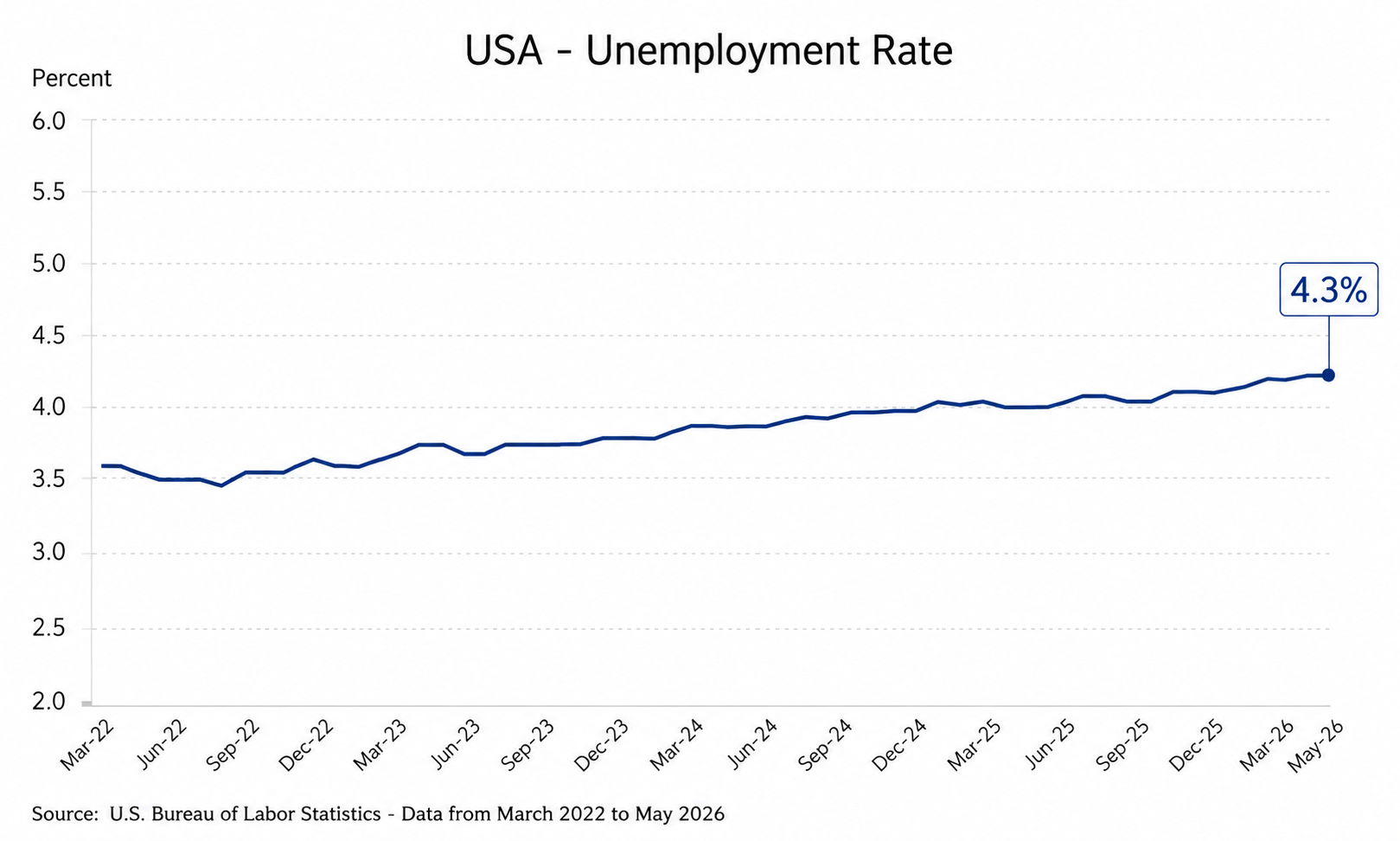

The labour market also supports the Federal Reserve’s cautious approach. Nonfarm payroll employment increased by 172,000 jobs in May, while the unemployment rate remained unchanged at 4.3%. Employment gains continued in sectors such as healthcare and leisure and hospitality, while federal government employment continued to decline. Average hourly earnings increased 0.4% during the month and were up 3.9% from a year earlier. While labour market conditions have become more balanced compared to the exceptionally tight conditions seen following the pandemic, employment growth remains solid and unemployment remains relatively low by historical standards. This suggests that the labour market is not currently weakening enough to create urgency for lower interest rates.

Source: U.S. Bureau of Labor Statistics - Unemployment Rate, March 2022 to May 2026

Global developments add another layer of uncertainty. The conflict in the Middle East has pushed energy prices higher and increased risks around global supply chains, which can raise costs for households and businesses while also weighing on global growth. Higher energy prices have been a key contributor to recent inflation data and remain an important risk for policymakers. At the same time, uncertainty surrounding global trade policy continues to affect business confidence, investment decisions, and financial markets. While the US economy has remained resilient, these external risks could influence both inflation and growth in the months ahead.

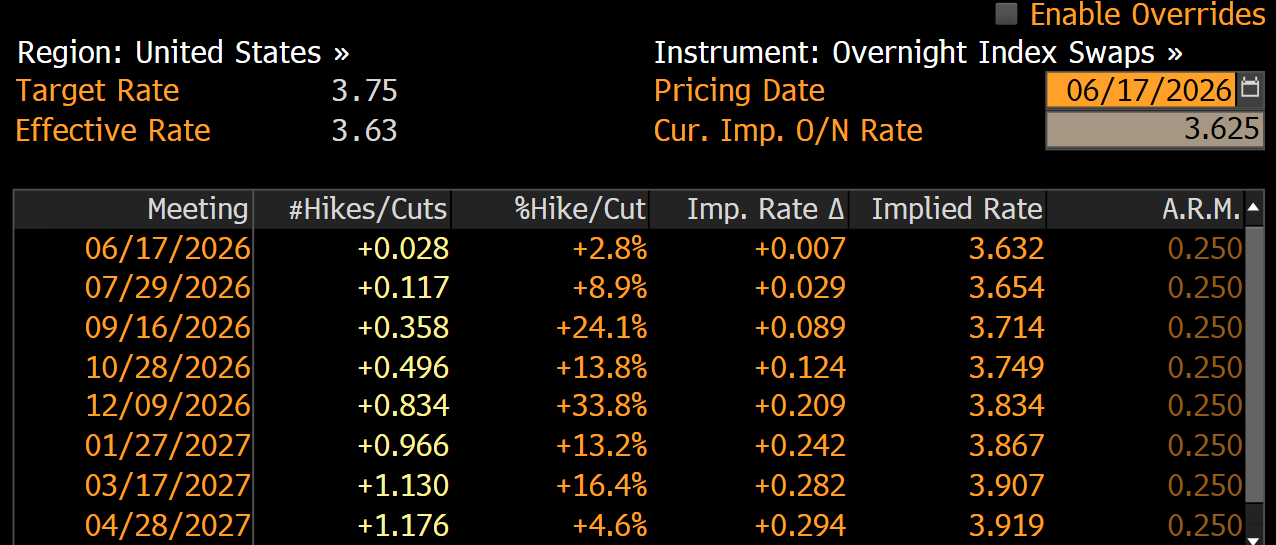

Looking ahead, the Federal Reserve’s next decisions will depend on whether inflation continues moving toward its target and whether economic activity begins to moderate. If inflation remains elevated, policymakers may need to maintain restrictive interest rates for longer than previously anticipated. Conversely, if inflation pressures ease and economic growth slows, the Fed could gain additional flexibility. Current market pricing suggests investors are increasingly expecting rates to remain higher for longer. As of June 17th, markets are assigning only an 8.9% probability of a rate increase at the July meeting. However, expectations for additional tightening rise later in the year, with markets pricing approximately 0.83 cumulative rate increases by the December meeting and more than one full rate increase by March 2027. These expectations will continue to evolve as new data becomes available, particularly around inflation, labour market conditions, economic growth, energy prices, and global trade developments.

World Interest Rate Probability - Source: Bloomberg - June 17, 2026

If you would like to discuss how these developments could affect your portfolio, please contact us at 604.643.0101 or cashgroup@cgf.com.

Book a meeting today with our of our advisors: https://calendly.com/cashgroup-cgf

Market Updates

Our market commentary breaks down the latest business, financial and money news. If you’d like to receive all of our market update emails, send us an email by clicking the subscribe button. If you found this content helpful, share it widely!