Bank of Canada Maintains Rate Hold as Inflation Rises and Growth Slows

On June 10th, the Bank of Canada announced that it is holding its overnight rate unchanged at 2.25%. The decision comes at a time when inflation has moved higher again, economic growth in Canada remains slow, and unemployment is still elevated compared to the levels seen in recent years. At the same time, geopolitical tensions in the Middle East have pushed energy prices higher, while uncertainty around US trade policy continues to weigh on the outlook for businesses, consumers, and investors.

Although the decision to hold rates steady was widely expected, the context behind it is important. The Bank of Canada is trying to assess whether the recent increase in inflation is mainly a temporary result of higher energy prices, or whether it could begin to affect prices more broadly across the economy. At the same time, softer economic growth gives the Bank a reason to be cautious about raising rates further.

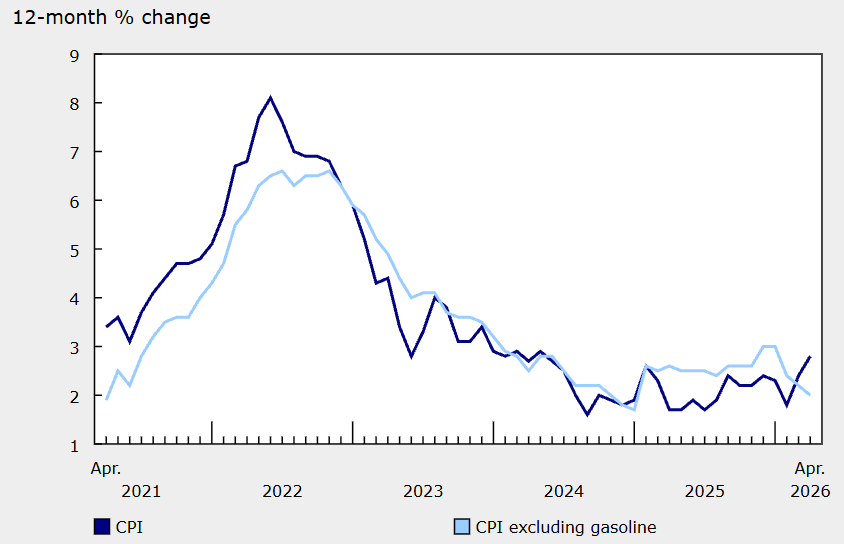

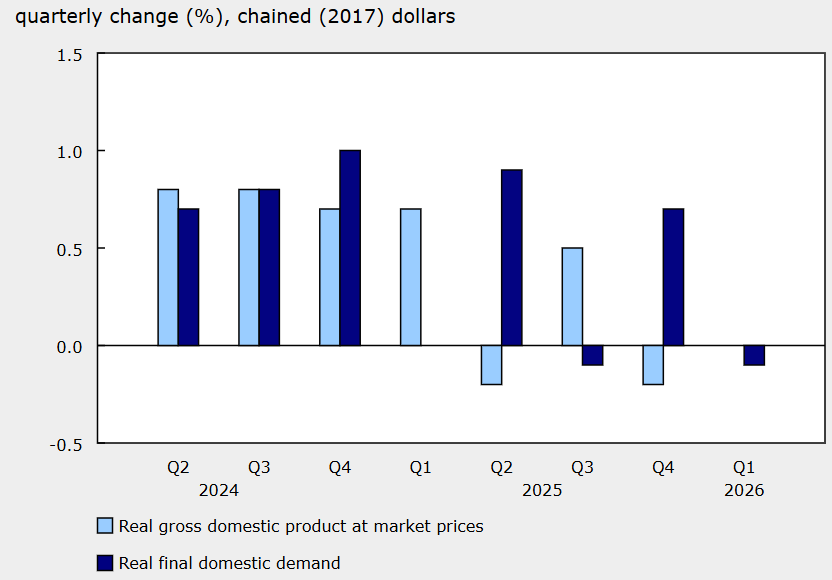

In April, Canada’s Consumer Price Index rose to 2.8%, up from 2.4% in March, with higher energy prices, particularly gasoline, driving the increase. Excluding gasoline, inflation was lower at 2.0%, suggesting that broader price pressures remain more contained than the headline number alone would imply. At the same time, the economy has lost momentum. The Bank noted that GDP decreased by 0.1% in the first quarter, which was weaker than it had expected in its April Monetary Policy Report. Consumer spending still increased, but this was not enough to offset weakness in other areas of the economy. Government spending decreased unexpectedly, housing activity declined, business investment remained weak, and exports fell. Imports also rose strongly as businesses rebuilt inventories.

Source: Statistics Canada - The 12-month change in the Consumer Price Index (CPI) and CPI excluding gasoline

Source: Statistics Canada - Real gross domestic product and final domestic demand

The labour market also supports a cautious approach. Employment increased by 88,000 in May, and the unemployment rate fell to 6.6% from 6.9% in April, which was a stronger monthly result than the earlier trend this year. However, the broader picture remains more balanced than strong. Statistics Canada noted that the May increase offset the downward trend observed from January to April, when full-time employment had declined. The Bank also noted that, looking through monthly movements, employment has changed little since the start of the year and the unemployment rate has generally remained in the 6.5% to 7% range. This suggests that the labour market is stable, but not tight enough to add significant inflation pressure on its own.

Global developments add another layer of uncertainty. The conflict in the Middle East has pushed energy prices higher and increased risks around global supply chains, which can raise costs for households and businesses while also weighing on global growth. For Canada, higher oil prices can support parts of the energy sector, but they also increase fuel costs and can keep headline inflation elevated. The US economy is also important to the outlook because it affects Canadian exports, business confidence, currency movements, and financial markets. While the US economy has remained more resilient than Canada’s, supported by consumer spending and investment, uncertainty around US trade policy continues to be a key risk for Canadian businesses, especially in trade-exposed sectors.

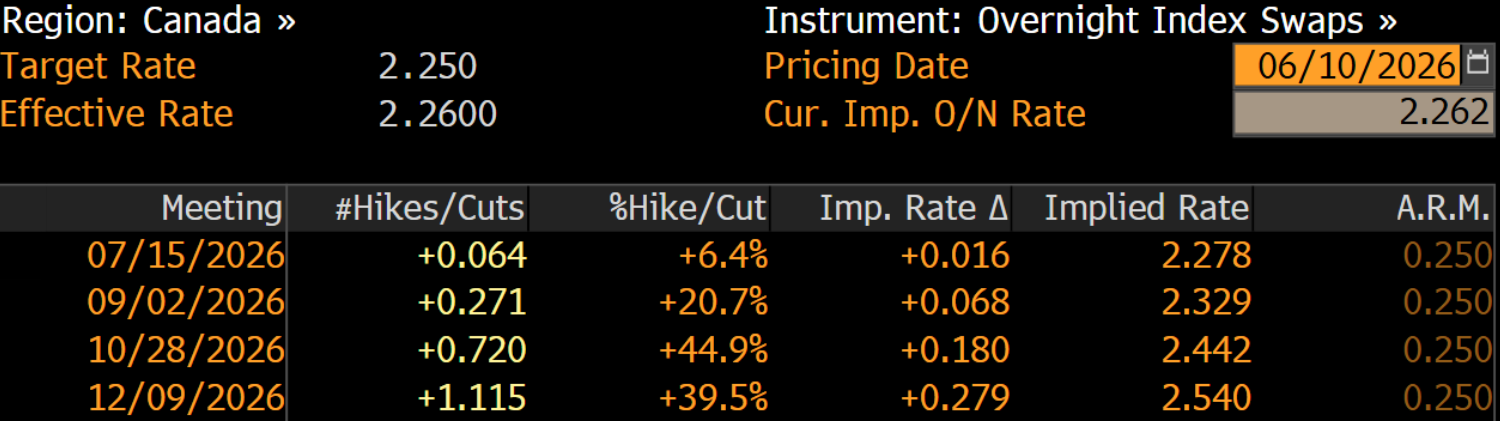

Looking ahead, the Bank’s next decisions will depend on whether inflation remains mainly concentrated in energy prices or begins to spread more broadly across the economy. If inflation pressures remain contained and growth stays soft, the Bank may have room to keep rates steady while it waits for more data. However, if higher energy prices become more persistent, or if inflation expectations begin to move higher, the Bank may need to maintain a more restrictive stance for longer. Current market pricing suggests that investors are not expecting an immediate rate increase. As of now, markets are assigning only a 6.4% probability of a 25 basis point rate increase at the Bank’s next meeting in July. Looking further ahead, the highest probability of a rate increase this year is currently assigned to the October meeting, at 44.9%. However, these expectations will continue to evolve as new economic data becomes available, particularly around inflation, growth, labour market conditions, energy prices, and the Canadian dollar.

World Interest Rate Probability - Source: Bloomberg - June 10, 2026

If you would like to discuss how these developments could affect your portfolio, please contact us at 604.643.0101 or cashgroup@cgf.com.

Book a meeting today with our of our advisors: https://calendly.com/cashgroup-cgf

Market Updates

Our market commentary breaks down the latest business, financial and money news. If you’d like to receive all of our market update emails, send us an email by clicking the subscribe button. If you found this content helpful, share it widely!