Understanding BC’s Credit Rating Downgrade

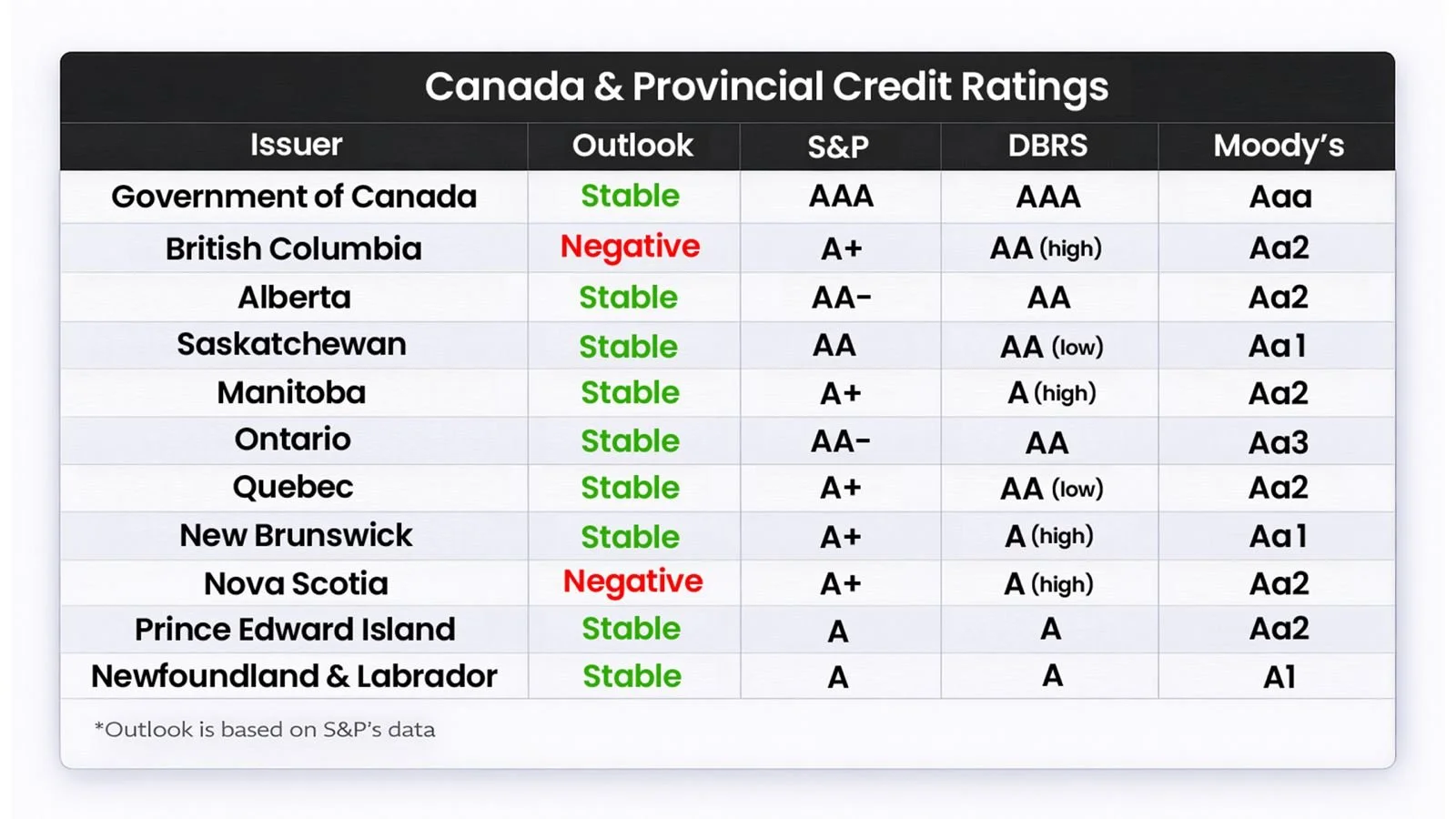

British Columbia’s credit rating has been downgraded again, marking the second consecutive downgrade by Moody’s and reinforcing a shift in the province’s fiscal position. The agency lowered BC’s long-term issuer and senior unsecured debt rating to Aa2 from Aa1, while maintaining a negative outlook. While credit ratings can appear technical, they play a direct role in shaping borrowing costs and provide an important signal about fiscal health.

This latest action builds on a series of changes over the past two years. In April 2024, Moody’s revised BC’s outlook to negative, reflecting growing concerns around the province’s fiscal trajectory. In April 2025, the province lost its Aaa rating and was downgraded to Aa1. The most recent downgrade to Aa2 suggests that the pressures identified earlier have not improved and, in some cases, have become more entrenched. What was initially viewed as a deterioration in outlook has now translated into a sustained decline in credit quality.

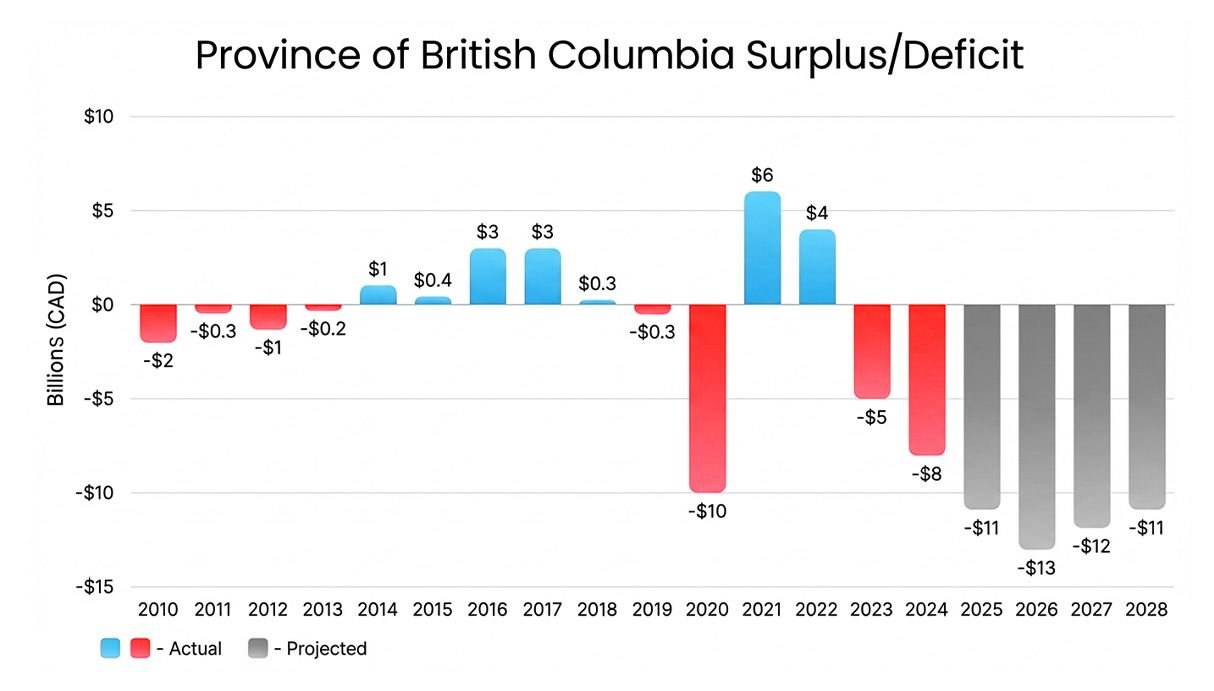

The downgrade reflects a combination of factors, most notably a continued widening of deficits and a rising debt burden. Government spending has increased across key areas, including healthcare, infrastructure, and housing, while revenue growth has not kept pace. As a result, the province is expected to run large deficits over the coming years, with no clearly defined path back to balance. BC’s fiscal plan projects a deficit of approximately $11 billion in 2025–26. Moody’s expects deficits to remain elevated in the following years, projecting deficits of $13.3 billion in 2026–27, $12.2 billion in 2027–28, and $11.4 billion in 2028–29. At the same time, debt levels are projected to rise significantly, with the debt-to-revenue ratio expected to exceed 250% in the coming years. Moody’s also pointed to a deterioration in fiscal management, indicating that current policies are not sufficient to stabilize the province’s financial position over the medium term.

Source: Financial Statements of the Province of British Columbia since 2010. BC Fiscal Plan 2025-26 to 2027-28. Moody’s Report as of March 19, 2026.

This trend becomes more apparent when looking at the trajectory of BC’s finances. As deficits persist, the province must continue issuing new debt to fund its operations, increasing its overall debt burden. At the same time, interest costs are rising as new borrowing is issued at higher rates than in previous years. This creates a compounding effect, where higher debt issuance leads to rising interest expenses, increasing the share of revenue allocated to debt servicing, which in turn contributes to larger deficits and necessitates further borrowing. Over time, this dynamic can become increasingly difficult to reverse, particularly if economic growth does not keep pace with the expansion in debt.

In a broader provincial context, BC has historically been viewed as one of the stronger credits in Canada, supported by a large and diversified economy. However, repeated downgrades suggest that it is moving away from the top tier of provincial issuers. While BC remains a high-quality borrower, it has moved below the strongest provincial credits, such as Saskatchewan and New Brunswick, which continue to benefit from relatively stronger fiscal positions and more stable debt trajectories. This divergence is becoming more relevant, as differences in credit quality begin to influence relative yields and risk across provincial bonds.

The implications of a lower credit rating are most clearly seen in borrowing costs. Credit ratings influence how investors assess risk, and in turn, the yield they require to lend. As a province’s credit profile weakens, investors typically demand higher yields to compensate for that additional risk. Over time, this can increase the cost of issuing new debt and refinancing existing obligations, raising overall interest expenses for the government. This dynamic does not operate in isolation. Higher borrowing costs reduce fiscal flexibility, as a larger share of government revenue must be allocated toward interest payments rather than public services or investment, while also limiting the province’s ability to respond to future economic downturns without further increasing debt.

For investors, these developments highlight the growing importance of provincial credit differentiation. As fiscal positions diverge, so too can yields across provincial issuers. Bonds issued by provinces facing greater fiscal pressure may offer higher yields, but also reflect a higher degree of credit risk relative to stronger issuers. In this environment, assessing relative value across provinces becomes more important, particularly within fixed income portfolios, as spreads between provincial issuers may continue to widen.

Looking ahead, the outlook remains negative, indicating that further downward pressure on the rating is possible if current trends persist. Stabilization would likely require a credible plan to reduce deficits and slow the pace of debt accumulation. Without such adjustments, the province’s borrowing costs may continue to rise, reinforcing the challenges already identified. Taken together, BC’s latest downgrade reflects more than a single rating change. It signals a broader shift in fiscal conditions, where persistent deficits, rising debt, and increasing interest costs are beginning to influence both credit quality and borrowing costs. For both policymakers and investors, this underscores the growing importance of fiscal discipline in an environment where financing conditions remain sensitive to changes in credit risk.

At the Cash Management Group, we continue to analyze central bank developments and their implications for clients. By staying ahead of policy shifts and maintaining a flexible, data driven approach, we help institutional and private clients navigate evolving market conditions with confidence.

If you would like to discuss how these developments could affect your portfolio, please contact us at 604.643.0101 or cashgroup@cgf.com.

Book a meeting today with our of our advisors: https://calendly.com/cashgroup-cgf

Market Updates

Our market commentary breaks down the latest business, financial and money news. If you’d like to receive all of our market update emails, send us an email by clicking the subscribe button. If you found this content helpful, share it widely!