Could You Access Your Wealth When It Matters Most?

Liquidity is often overlooked in portfolio construction, yet it plays a critical role in how effectively wealth can be used when needed. While many investors focus on returns and diversification, the ability to access capital without disrupting a long-term plan is equally important. This becomes particularly relevant during periods of market stress, when the timing of withdrawals can have a meaningful impact on outcomes.

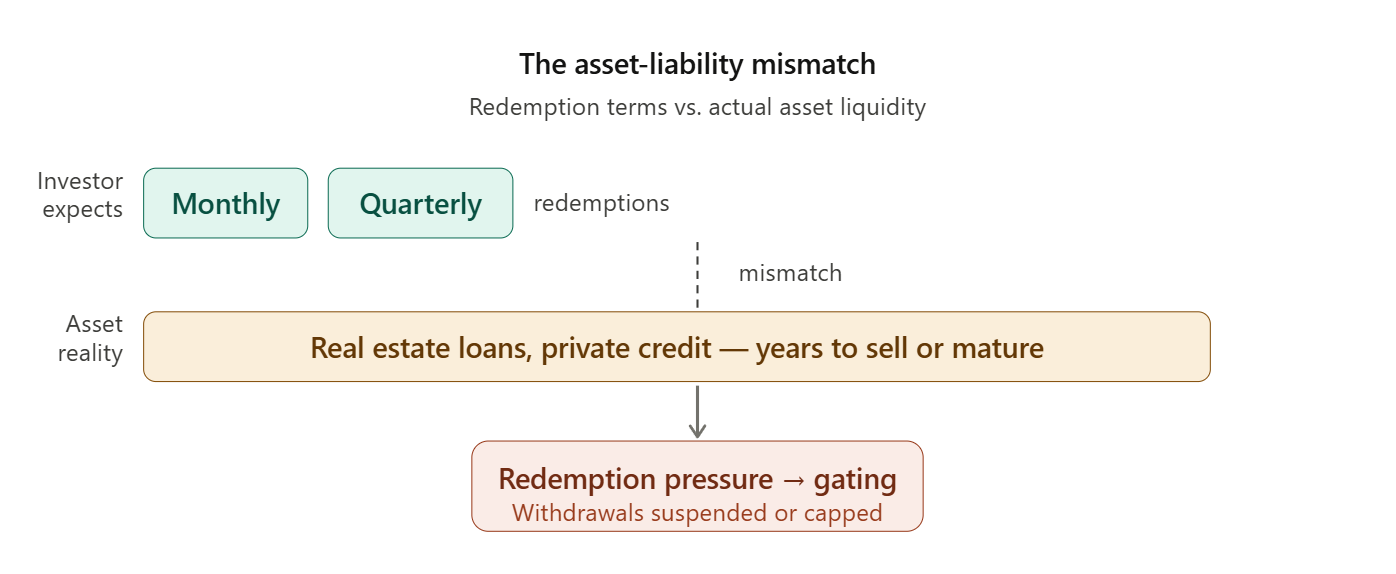

In public markets, liquidity is often taken for granted. Stocks and exchange traded funds can typically be sold quickly, reinforcing the perception that portfolios are fully flexible. However, as portfolios incorporate private investments such as real estate, private credit, or infrastructure, the relationship between portfolio value and usable capital becomes more complex. In these cases, liquidity is not always immediate, and access to capital may depend on specific terms, notice periods, or market conditions.

This distinction between owning wealth and being able to use it is where liquidity risk emerges. A portfolio can appear well diversified and substantial in value, yet still lack the flexibility required to meet real-world cash needs without forcing suboptimal decisions.

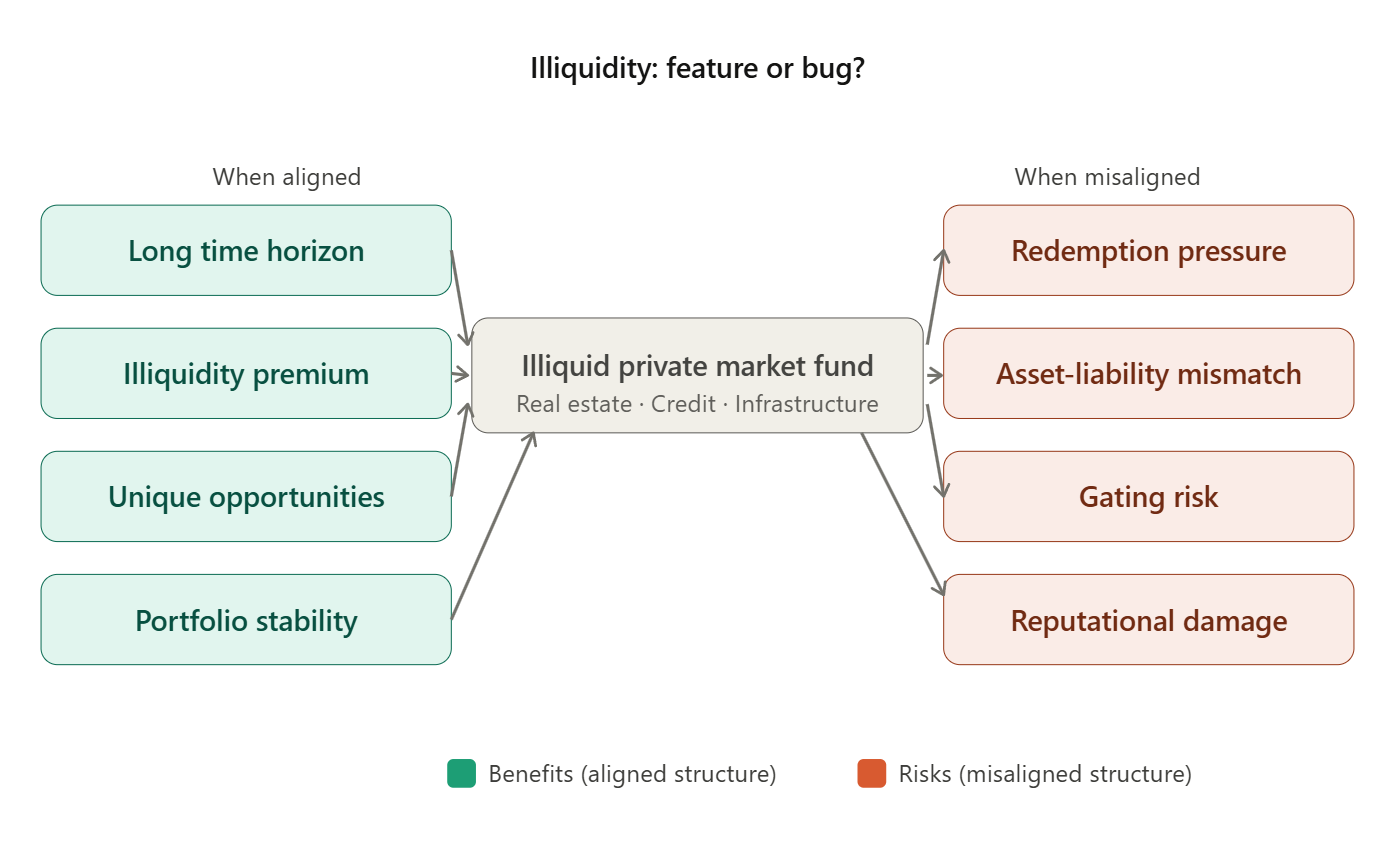

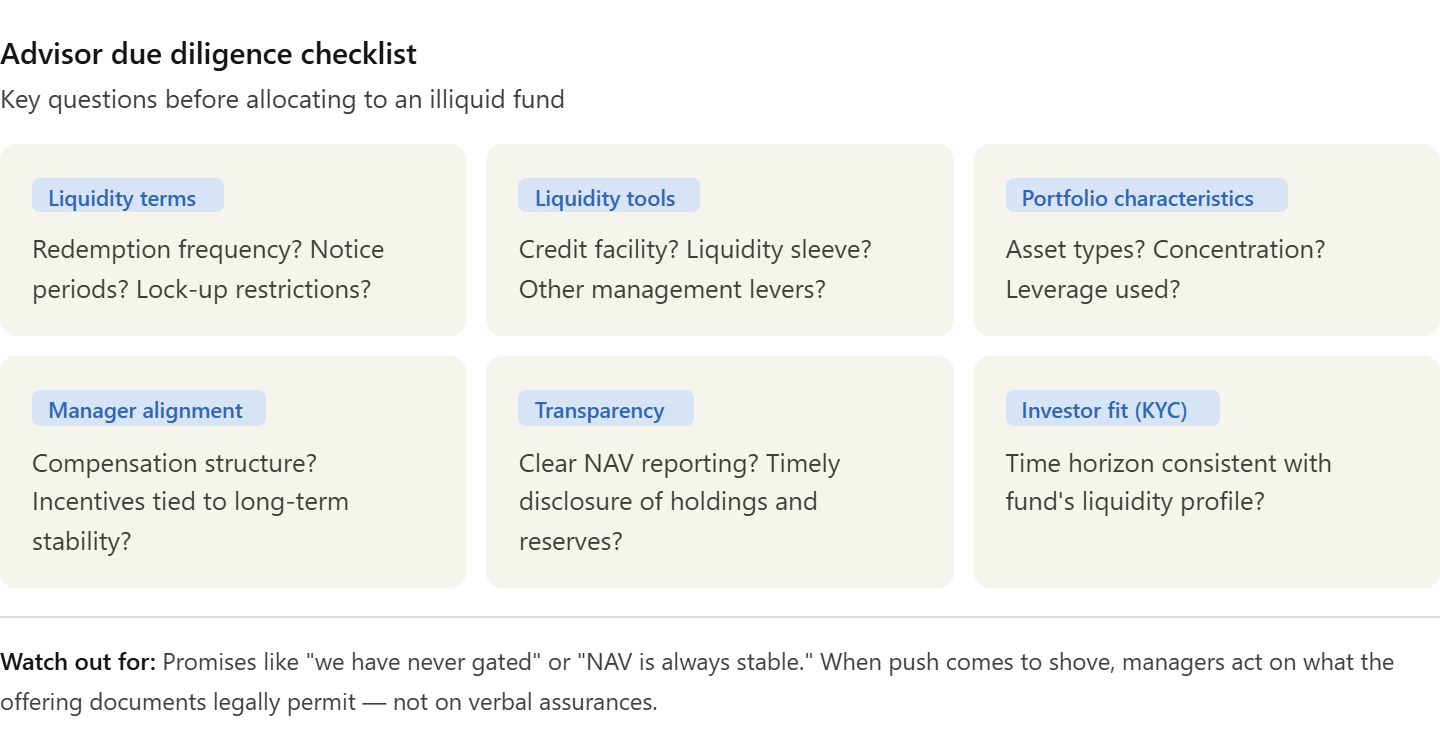

Recent developments in private markets have highlighted this dynamic. Certain funds have implemented redemption limits or delayed withdrawals in response to increased investor demand for liquidity. While these measures are often aligned with protecting long-term value, they can create a mismatch between investor expectations and the underlying structure of the investment. This reinforces the importance of understanding liquidity terms before allocating capital, rather than assuming access will always be available.

At the same time, illiquidity is not inherently a disadvantage. In many cases, it is a deliberate feature of private investments. Longer-term capital allows managers to focus on value creation without the pressure of short-term market movements, and may provide access to opportunities not available in public markets. Investors may also benefit from an illiquidity premium as compensation for committing capital over longer time horizons. However, these benefits must be balanced against the need for flexibility, particularly when capital may be required unexpectedly.

The impact of liquidity becomes more pronounced when timing matters. Portfolios rarely experience stress due to a lack of return potential. More often, challenges arise when capital is needed during periods of market weakness. This is particularly relevant for investors approaching retirement, drawing income, or relying on their portfolio to support ongoing lifestyle decisions. In these cases, the sequence of returns and the timing of withdrawals can have a lasting effect on long-term outcomes.

In practice, liquidity challenges often lead to unintended consequences. Investors may sell liquid assets simply because they are accessible, while less liquid holdings remain in place. If markets recover, the assets that were sold may have been the ones best positioned to rebound, leaving the portfolio less flexible and potentially weaker than before. This highlights that liquidity is not only about access, but about preserving the ability to make informed decisions.

A more structured approach to liquidity can help address these risks. One effective framework is to segment capital based on time horizon and purpose. Near-term needs, such as living expenses, tax obligations, or planned purchases, can be allocated to highly liquid assets designed to provide stability. A second layer of capital can be positioned to provide flexibility, allowing investors to respond to changing conditions without being forced to act. Longer-term capital, which is not required in the near future, can then be allocated to less liquid strategies where time horizon and structure are aligned.

This separation allows each portion of the portfolio to serve a specific role, reducing the likelihood that long-term investments are disrupted by short-term needs. It also reinforces a key principle in wealth management: different dollars have different jobs, and should be managed accordingly.

Ultimately, liquidity is not simply a technical feature of an investment. It is a core component of portfolio design that influences how effectively capital can support real life decisions. While central to private markets, liquidity considerations extend across all asset classes, including concentrated positions, real estate holdings, and traditional portfolios with insufficient accessible cash.

Taken together, these dynamics highlight that a well constructed portfolio is not defined solely by its return potential, but by its ability to function when timing becomes unfavourable. Ensuring that capital is both invested effectively and accessible when needed is essential to maintaining flexibility, preserving long-term value, and supporting the broader objectives of wealth.

At the Cash Management Group, we stay ahead of policy shifts and maintain a flexible, data-driven approach. We help institutional and private clients navigate evolving market conditions with confidence.

If you would like to discuss how these developments could affect your portfolio, please contact us at 604.643.0101 or cashgroup@cgf.com.

Book a meeting today with our of our advisors: https://calendly.com/cashgroup-cgf

Market Updates

Our market commentary breaks down the latest business, financial and money news. If you’d like to receive all of our market update emails, send us an email by clicking the subscribe button. If you found this content helpful, share it widely!