BoC and FED Pause as Markets Navigate the Effects of the Middle East Conflict

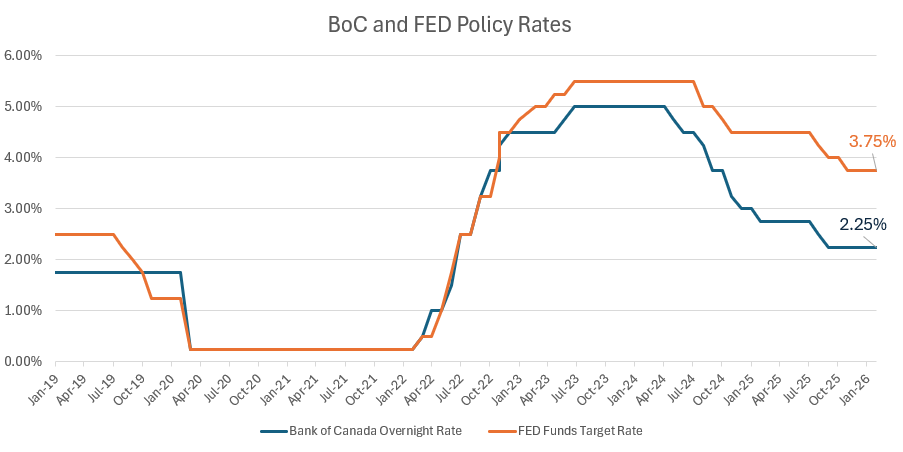

On March 18th, both the Bank of Canada and the U.S. Federal Reserve announced that they are holding their policy rates steady, a decision that comes during the times of heightened economic uncertainty and ongoing geopolitical tensions in the Middle East. The Bank of Canada maintained its overnight rate at 2.25%, a level unchanged since October 29, 2025, while the Federal Reserve kept its target range at 3.50%–3.75%, where it has stood since December 11, 2025. These decisions reflect a cautious stance by both central banks as they balance signs of slowing economic momentum with renewed inflation risks linked to recent energy market volatility and broader global instability.

Looking more closely at inflation, recent data continue to show a divergence between Canada and the United States. In Canada, year‑over‑year CPI eased to 1.8% in February, down from 2.3% in January, partly reflecting base‑year effects related to the expiration of the temporary GST/HST break last February, which had boosted prices at that time. Despite this moderation, underlying pressures remain, with restaurant food prices still rising 7.8% year over year and grocery prices increasing 4.1%, while gasoline prices, though down on a year‑over‑year basis, rose on a monthly basis due to higher crude oil prices due to the Middle East conflict and supply disruptions. In contrast, U.S. inflation remained steady, with February headline CPI rising 2.4% year over year, unchanged from January, as increases in shelter costs, energy prices, and food continued to drive the overall reading, alongside price gains in categories such as medical care, education, apparel, and airline fares.

Labour market conditions also paint a mixed picture across the two economies. In Canada, February data surprised to the downside, with the economy shedding 84,000 jobs and the unemployment rate rising to 6.7%, following job losses and a smaller uptick in unemployment already recorded in January. Employment declines were concentrated among youth and men in the core working age of 25 to 54 years old, with notable weakness in wholesale and retail trade. In the U.S., labour market softening has been more gradual, as nonfarm payroll employment declined by 92,000 in February leaving the unemployment rate mostly unchanged at 4.4%, following a solid job gain in January, with ongoing declines seen in sectors such as health care, information, and federal government employment.

So far, traditional economic indicators like inflation and unemployment have yet to capture the effects of recent geopolitical developments. In recent weeks, tensions in the Middle East have escalated after the U.S. launched joint strikes with Israel against Iran’s ruling regime, focusing on its military, missile, and nuclear infrastructure following a breakdown in diplomacy. In response, Iran has taken actions that have affected regional shipping routes, particularly around the Strait of Hormuz, which has raised concerns about global oil supply and contributed to increased energy price volatility. The Strait of Hormuz is especially important because roughly a fifth of the world’s oil trade passes through this narrow waterway each day, making any disruption there highly impactful for global energy markets. As a result, oil buyers are seeking alternative sources outside the Gulf, pushing prices higher for crude grades globally, from Europe to Central Asia, and driving benchmark oil prices in Oman to record levels.

In Canada and the U.S., the conflict has already led to higher oil and natural gas prices, which central banks expect will add to inflation in the near term. Shipping disruptions also risk constraining supplies of other key commodities such as fertilizer, which could put upward pressure on food prices over time. At the same time, financial conditions have tightened, with higher global bond yields, weaker equity markets, and wider credit spreads, although the Canada–U.S. dollar exchange rate has remained relatively stable so far. What has stood out so far is that equity markets have been more resilient than many initially expected as the conflict intensified. While markets did decline, they rebounded relatively quickly, and the overall impact has so far been more muted than was widely anticipated.

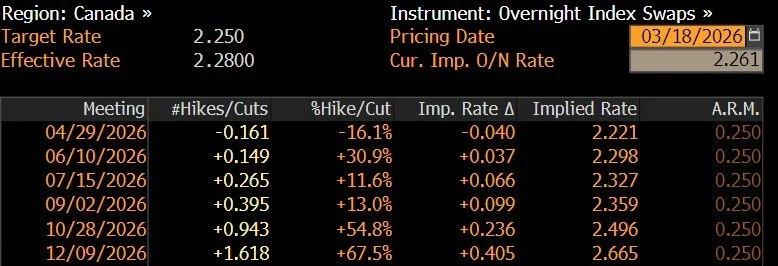

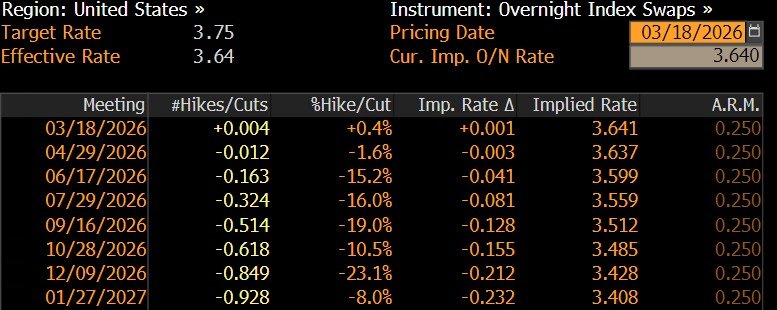

Since the conflict intensified, market expectations for U.S. interest‑rate cuts in the second half of 2026 have eased. Currently, markets are largely pricing in stable rates, with only about a 20% probability of a cut later in the year. In Canada, the outlook is somewhat different, with markets now leaning toward further tightening after June 2026—implying a 54.8% probability of a rate increase in October and a 67.5% probability by December. These expectations are likely to continue evolving as the economic effects of the conflict become clearer over time.

At the Cash Management Group, we continue to analyze central bank developments and their implications for clients. By staying ahead of policy shifts and maintaining a flexible, data driven approach, we help institutional and private clients navigate evolving market conditions with confidence.

World Interest Rate Probability - Source: Bloomberg - March 18, 2026

If you would like to discuss how these developments could affect your portfolio, please contact us at 604.643.0101 or cashgroup@cgf.com.

Book a meeting today with our of our advisors: https://calendly.com/cashgroup-cgf

Market Updates

Our market commentary breaks down the latest business, financial and money news. If you’d like to receive all of our market update emails, send us an email by clicking the subscribe button. If you found this content helpful, share it widely!